Accrual Basis Accounting Explained provides the essential framework for accurately diagnosing a company’s financial health. By covering everything from the definition of accrual accounting to revenue recognition timing and complex accounting principles, this guide delivers reliable information that is immediately applicable to both practice and theory.

Table of Contents

- Definition and Basic Concepts of Accrual Accounting

- Accrual Basis Accounting Explained: 5 Core Operating Principles

- Key Differences Between Accrual and Cash Basis Accounting

- Specific Application Examples of Revenue and Expense Recognition

- How to Verify Accounting Standards via Official Institutions

- Strategic Implementation of Accrual Basis Accounting Explained

Definition and Basic Concepts of Accrual Accounting

Accrual basis accounting is a fundamental principle that records revenues and expenses when an economic event occurs, regardless of when cash actually changes hands. This method is designed to represent a company’s financial performance most accurately within a specific period.

The Financial Accounting Standards Board (FASB) and International Financial Reporting Standards (IFRS) require or strongly recommend that companies apply accrual accounting when submitting reports to external stakeholders. From the perspective of Accrual Basis Accounting Explained, this method focuses on the moment a service is rendered or goods are delivered, rather than simply when money moves. This allows management to understand current performance without the distortion of cash flow timing.

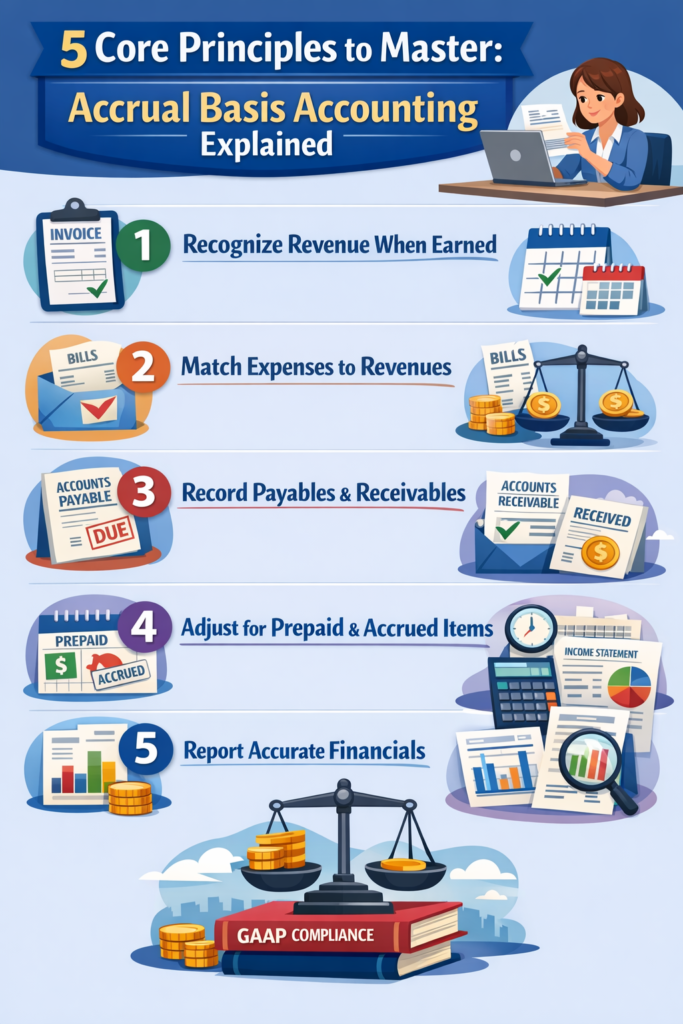

Accrual Basis Accounting Explained: 5 Core Operating Principles

To correctly implement accrual accounting, one must master these five mechanisms. Each principle serves to increase the reliability of financial statements.

1. Revenue Recognition Principle

Revenue is recognized when the revenue-generating process is complete—meaning goods or services have been delivered to the customer—not necessarily when payment is received.

2. Matching Principle

Expenses incurred to generate revenue must be recorded in the same accounting period as the corresponding revenue. This is the core logic behind aligning COGS (Cost of Goods Sold) with Sales.

3. Accrued Expenses and Revenues

At the end of a fiscal year, expenses that have occurred but have not yet been paid (e.g., Interest Payable) or revenues earned but not yet received (Accrued Revenue) are reflected to ensure an accurate closing.

4. Deferrals (Prepaid Expenses and Unearned Revenue)

Insurance premiums paid in advance or contract deposits received are not current period expenses or revenues. These are held as assets or liabilities until the actual period of use arrives.

5. Depreciation and Amortization

The cost of a tangible asset is not expensed all at once. Instead, it is allocated across the useful life during which the asset contributes to revenue generation.

Key Differences Between Accrual and Cash Basis Accounting

Accrual and cash basis accounting differ significantly at the point of transaction recording. The table below compares the characteristics of Accrual Basis Accounting Explained.

| Category | Accrual Basis Accounting | Cash Basis Accounting |

| Revenue Recognition | When service is provided/rights arise | When cash is received |

| Expense Recognition | When expense occurs/revenue is matched | When cash is paid |

| Main Advantage | Accuracy in measuring performance | Simplicity and ease of cash tracking |

| Financial Statements | Balance Sheet & Income Statement required | Focus on Cash Flow analysis |

| Primary Target | Corporations, large businesses, public companies | Small business owners, sole proprietors |

Note: These criteria may vary depending on national accounting regulations and company size. For detailed information, please refer to official announcements from the U.S. Department of the Treasury.

Specific Application Examples of Revenue and Expense Recognition

Revenue Recognition in Accrual Accounting

If a software company sells an annual subscription in December and receives the full payment, cash basis accounting records the total revenue in December. However, under accrual principles, only one month of revenue is recognized in December, while the remaining 11 months are recorded as a liability (Unearned Revenue) and deferred to the following year.

Expense Matching Example

Raw material costs used to produce a product are recognized as an expense (COGS) only when the product is actually sold. If the product remains in the warehouse, it is classified as an asset (Inventory) rather than an expense. This sophisticated treatment is the value added by Accrual Basis Accounting Explained.

FAQ: Frequently Asked Questions

Is accrual accounting always better than cash basis?

While accrual accounting is superior in terms of information depth and accuracy, it can be complex for very small businesses. The choice depends on company size and disclosure obligations.

Must I use accrual accounting for tax reporting?

Many tax authorities require businesses above a certain revenue threshold to file taxes based on accrual accounting. However, because tax law and accounting standards can differ, professional consultation is advised.

How do I check cash flow in accrual accounting?

Accrual ledgers alone make it difficult to see actual cash on hand. Therefore, it is essential to analyze the “Statement of Cash Flows” alongside other statements to track actual cash movements.

How to Verify Accounting Standards via Official Institutions

Accounting policies and standards can be updated annually or vary by industry. To verify accurate regulations regarding Accrual Basis Accounting Explained, we recommend the following steps:

- Utilize Official Government Portals: Check accounting guidelines published by public institutions and government departments.

- Search Official Press Releases: Policy changes or tax law revisions are found fastest in the “Announcements” or “Press Release” sections of institutional websites.

- Seek Professional Advice: For specific application scopes or eligibility, verify the latest disclosure standards through a Certified Public Accountant (CPA).

- Verify Domain Authenticity: When searching for information, ensure the website address ends in .gov or .org to confirm it is a trusted institution.

Strategic Implementation of Accrual Basis Accounting Explained

Adopting and maintaining accrual accounting is more than just following regulations—it is the path to securing long-term financial health. When applying Accrual Basis Accounting Explained in practice, you must strictly manage the timing of revenues and expenses and develop a habit of reconciling receivables and payables through monthly closing procedures.

Furthermore, strengthening internal control systems reduces the gap between actual transactions and ledger records. These efforts form the basis for gaining high trust from investors and financial institutions and enable rational decision-making based on data.

We recommend regularly monitoring guidelines from authoritative bodies such as the American Institute of Certified Public Accountants (AICPA) to respond flexibly to policy changes.

This article is for informational purposes only. Consult a licensed CPA or accounting professional for personalized advice.