Mastering Cash Basis Accounting is critical for small business owners and self-employed professionals seeking a straightforward way to track financial health. This guide provides a verified 5-step framework based on federal tax guidelines to help you record income, manage expenses, and maintain compliance while ensuring your bookkeeping aligns with official public institution standards.

Table of Contents

- Understanding the Core of Mastering Cash Basis Accounting

- Eligibility and Usage Rules for Small Businesses

- 5 Strategic Steps for Mastering Cash Basis Accounting

- Key Differences: Cash vs. Accrual Methods

- Compliance Precautions and Verification Methods

- Frequently Asked Questions (FAQ)

- Final Checklist for Mastering Cash Basis Accounting

1. Understanding the Core of Mastering Cash Basis Accounting

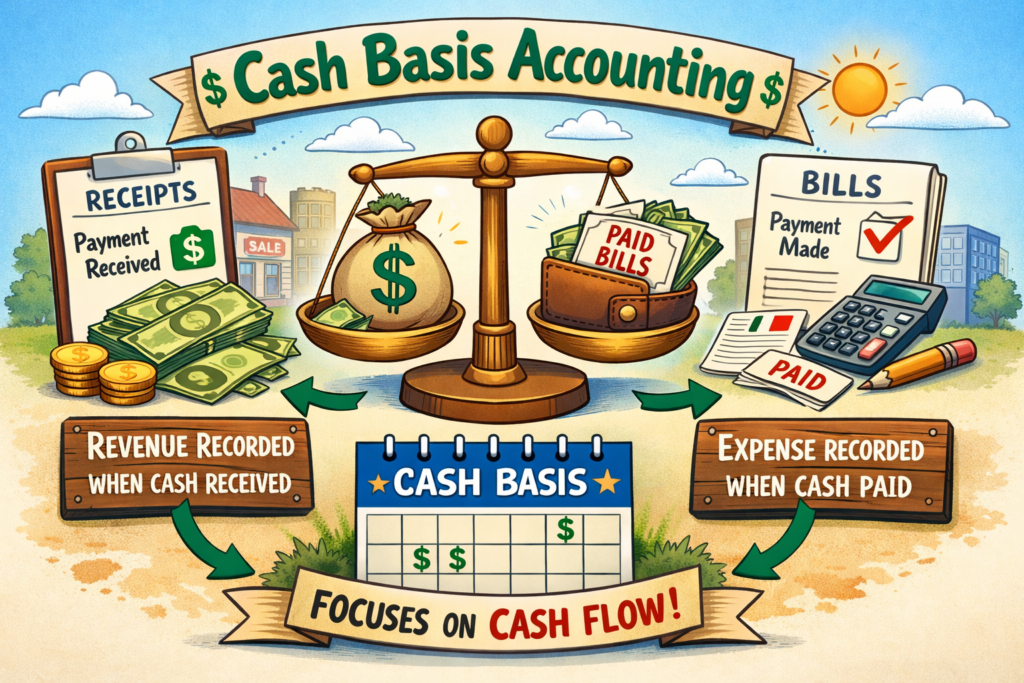

Cash basis accounting is a financial recording method where revenue is recognized only when cash is received, and expenses are recorded only when they are actually paid. Unlike the accrual method, which records transactions when they are earned or incurred, this approach focuses on actual liquid cash flow.

To truly succeed in Mastering Cash Basis Accounting, one must understand the “Constructive Receipt” doctrine. According to official tax principles, income is considered received when it is credited to your account or made available for your use without restriction, even if you haven’t physically collected the cash yet.

2. Eligibility and Usage Rules for Small Businesses

Not every entity is permitted to use this simplified method. Eligibility often depends on the nature of the business and its annual gross receipts.

- Gross Receipts Test: Generally, small businesses and statutory individuals whose average annual gross receipts for the prior three years do not exceed a specific inflation-adjusted threshold are eligible.

- Entity Type: Sole proprietorships, S-Corporations, and certain partnerships typically find this method most accessible.

- Inventory Restrictions: Historically, businesses with significant inventory were required to use accrual; however, updated policies may allow certain small businesses to treat inventory as non-incidental materials and supplies under the cash method.

Note: Eligibility criteria may vary depending on the tax year or specific policy updates. Please confirm the latest thresholds through official government announcements.

3. 5 Strategic Steps for Mastering Cash Basis Accounting

Step 1: Verify Qualification

Before implementation, consult official public institution guidelines to ensure your business meets the current gross receipts test. This prevents future penalties during audits.

Step 2: Establish a Real-Time Recording System

Since timing is everything, you must record income on the exact date the check is received or the electronic transfer hits your account. Delayed entry can lead to inaccurate fiscal year reporting.

Step 3: Align Expenses with Payments

Record business expenses only when the funds leave your account. For credit card transactions, the expense is generally deductible in the year the charge is made, not necessarily when the credit card bill is paid.

Step 4: Perform Monthly Bank Reconciliation

Compare your ledger against official bank statements. This ensures that every “cash” event in the real world is reflected in your accounting software, which is a cornerstone of Mastering Cash Basis Accounting.

Step 5: Monitor for “Method Change” Triggers

As a business grows, it may exceed the allowable revenue limit for cash accounting. You must be prepared to file the necessary official forms to transition to the accrual method if you surpass these limits.

4. Key Differences: Cash vs. Accrual Methods

| Category | Cash Basis | Accrual Basis |

| Revenue Recognition | When cash is received | When service/product is provided |

| Expense Recognition | When bill is paid | When expense is incurred |

| Complexity | Low (Simple to maintain) | High (Requires advanced tracking) |

| Cash Flow Visibility | Excellent | Indirect |

| Typical User | Small business/Service-based | Large corporations/Inventory-heavy |

5. Compliance Precautions and Verification Methods

While simplicity is a benefit, precision is required to avoid “mismatching” income and expenses in a way that triggers an audit.

- Prepaid Expenses: You generally cannot deduct an entire multi-year insurance premium in one year, even if paid in full. The “12-month rule” often applies, where the deduction is limited to the portion of the benefit consumed within the tax year.

- Consistency: Once you choose a method, you must use it consistently. Changing methods usually requires formal approval from the national tax authority.

How to Independently Verify Rules (Verification Guidance)

To ensure your practices are up to date, you should independently verify eligibility and usage rules by:

- Accessing the official website of your national or regional tax authority.

- Searching for “Publication 538” or “Accounting Periods and Methods” in the official search bar.

- Reviewing the latest “Gross Receipts Test” updates for the current tax year to see if your business still qualifies for the cash method.

6. Frequently Asked Questions (FAQ)

Can I track Accounts Receivable in cash basis?

Technically, no. In Mastering Cash Basis Accounting, an invoice sent to a client is not recorded in the general ledger until the payment is received. However, you should keep a separate “pro-forma” list for management purposes.

What happens if I receive a check on Dec 31 but deposit it on Jan 2?

Under the Constructive Receipt rule, that income is generally recognized in the year the check was made available to you (the year ending Dec 31).

Is this method allowed for corporations?

Only if they meet the specific gross receipts threshold set by the government. Large C-Corporations are typically required to use the accrual method.

7. Final Checklist for Mastering Cash Basis Accounting

To achieve full proficiency in Mastering Cash Basis Accounting, your next step should be a thorough audit of your current transaction logs. Ensure that no “earned but unpaid” revenue has accidentally inflated your current year’s profit figures.

Maintain a rigorous archive of digital and physical receipts to support every cash outflow recorded. By staying informed through official public institution portals and monitoring your annual turnover, you can ensure your accounting method remains both legal and beneficial for your business’s growth.

External Resources:

This article is for informational purposes only. Consult a licensed CPA or accounting professional for personalized advice.