An S Corporation combines the legal liability protection of a corporation with the tax efficiency of a partnership, offering a rational tax structure that prevents double taxation. Based on official regulations from the Internal Revenue Service (IRS), this document details the eligibility requirements for S Corporation conversion, essential procedures, and a comparative analysis against other business entity types.

Table of Contents

- Definition and Purpose of an S Corporation

- Comparative Analysis of Business Entities

- 5 Key Eligibility Requirements for S Corporation Formation

- S Corp Conversion Process and Form 2553

- Operational Cautions and Reasonable Salary

- Frequently Asked Questions (FAQ)

- How to Verify and Validate Official Information

- Conclusion for Successful S Corporation Operation

Definition and Purpose of an S Corporation

An S Corporation refers to a corporate structure that is taxed under Subchapter S of the Internal Revenue Code by the IRS. Unlike a standard C Corporation, which has a “double taxation” structure where taxes are paid once at the corporate level and again at the shareholder level on dividends, an S Corporation has a “pass-through” structure where profits and losses are passed through to the shareholders’ personal income, and only personal income tax is paid.

This structure is primarily utilized by small business owners to maximize tax efficiency and reduce self-employment tax. However, not every business can choose to be an S Corporation; strict eligibility requirements must be met.

Comparative Analysis of Business Entities

Before considering converting to an S Corporation, it is crucial to clearly understand how it differs from other business entities. The table below compares key features based on IRS and Small Business Administration (SBA) standards.

| Category | S Corporation | C Corporation | LLC (Limited Liability Company) |

| Taxation Method | Pass-through: No corporate tax; shareholders pay personal income tax. | Double Taxation: Corporate tax is paid first, then shareholders pay tax on dividends. | Pass-through: Default taxation as partnership/sole proprietorship (can elect to be taxed as an S Corp or C Corp). |

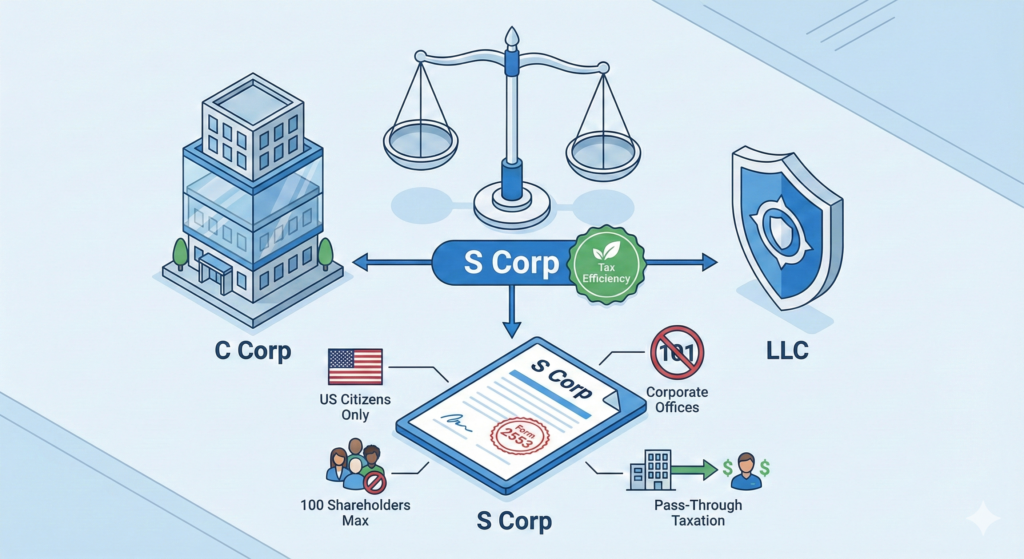

| Ownership Limits | Strict: Max 100 shareholders; must be US residents/citizens (foreigners not allowed). | No Limits: Unlimited number of shareholders; foreign ownership permitted. | No Limits: Unlimited number of members; foreign ownership permitted. |

| Stock Type | Can only issue one class of stock (Common Stock). Differences in voting rights are permitted. | Can issue various classes of stock (preferred, common, etc.). | Concept of Membership Interest, not stock. |

| Self-Employment Tax | Tax Saving Effect: Income exceeding “reasonable salary” is treated as distributions and exempt from self-employment tax. | Not applicable (salary and dividend income). | All net earnings are subject to self-employment tax (unless S Corp taxation is elected). |

Analysis and Selection Guide

- When an S Corporation is favorable: You are a US resident, and the business generates profit above a certain level, making self-employment tax reduction necessary.

- When a C Corporation is favorable: You plan to attract venture capital investment, aim for an initial public offering (IPO) in the future, or have foreign investors.

- When an LLC is favorable: You desire a flexible management structure or asset protection is key, such as in real estate investment.

5 Key Eligibility Requirements for S Corporation Formation

The IRS mandates that the following requirements must be met to qualify as an S Corporation. If even one is violated, the qualification may be revoked.

- Domestic Corporation: It must be a corporation organized in the United States.

- Shareholder Eligibility Restrictions: Shareholders must be individuals, certain trusts, or estates. Partnerships, other corporations, or non-resident aliens cannot be shareholders.

- Limit on Number of Shareholders: The number of shareholders cannot exceed 100. (Family members can be treated as one shareholder under certain conditions).

- Limit on Stock Classes: It must have only one class of stock. However, differences in voting rights solely are permitted.

- Ineligible Corporations Excluded: Certain financial institutions, insurance companies, and domestic international sales corporations (DISCs) cannot be S Corporations.

S Corp Conversion Process and Form 2553

Creating an S Corporation is not a separate incorporation process; rather, it is a request by an existing C Corporation or LLC to the IRS to ‘change its tax status’.

1. Filing Form 2553

To obtain S Corporation status, you must complete and submit Form 2553 (Election by a Small Business Corporation) to the IRS. This form requires the consent signatures of all shareholders.

2. Time Requirements for Filing

The timing of the application is critical. To be effective for the current tax year, it must be filed during one of the following two periods:

- Within 2 months and 15 days after the beginning of the tax year.

- At any time during the preceding tax year.

Caution: If you miss the deadline, you may need to request ‘Late Election Relief’, which requires explaining the reason for the delay.

Operational Cautions and Reasonable Salary

The most crucial point to watch when operating an S Corporation is setting a ‘Reasonable Salary’.

- IRS Regulation: A shareholder-employee of an S Corporation must receive reasonable compensation corresponding to market averages for the services they provide.

- Risk Factors: If you set a salary too low to reduce self-employment tax and take the remaining profits as distributions, you may become subject to an IRS audit. The IRS considers this tax evasion and may recharacterize distributions as wages, imposing substantial penalties and interest.

- Recommendation: Determine salary based on average wage data for the industry, region, and job role, and keep records.

Frequently Asked Questions (FAQ)

Can a foreigner own an S Corporation?

No, it is impossible. Shareholders of an S Corporation must be US citizens or resident aliens. If a non-resident alien is a shareholder, S Corp status cannot be obtained.

Can an LLC also become an S Corporation?

Yes, it is possible. An LLC is a legal limited liability company, but for tax purposes, it can elect S Corporation taxation by filing Form 2553. Through this, it can enjoy both the legal protection of an LLC and the tax benefits of an S Corp.

What happens if I miss the S Corporation application deadline?

In principle, the status will remain a C Corporation (or default LLC taxation) for that year. However, the IRS operates a system designed to provide relief for late elections if there is reasonable cause. You can request relief by stating the reason for missing the deadline when filing Form 2553.

How to Verify and Validate Official Information

Tax laws change annually, so you must verify the latest announcements from official agencies.

- Eligibility Requirements and Forms: Search for

Form 2553andInstructions for Form 2553on the official IRS website. - Small Business Regulations: Check the Business Structure section on the U.S. Small Business Administration (SBA) website.

- Salary Standards: Validate ‘reasonable salary’ levels by referring to wage data from sources like the U.S. Bureau of Labor Statistics (BLS).

Verification Tip: Make sure the source domain ends in .gov. Information from blogs or forums should be used for reference only.

Review for Successful S Corporation Operation

We have examined the definition, eligibility requirements, and comparative analysis of the S corporation. An S Corp offers significant tax savings when utilized appropriately, but strict adherence to eligibility requirements and salary regulations is necessary. Base your decisions on a careful review of this guide and official IRS information to determine the best path for your business growth.

This article is for informational purposes only. Consult a CPA for personalized advice.